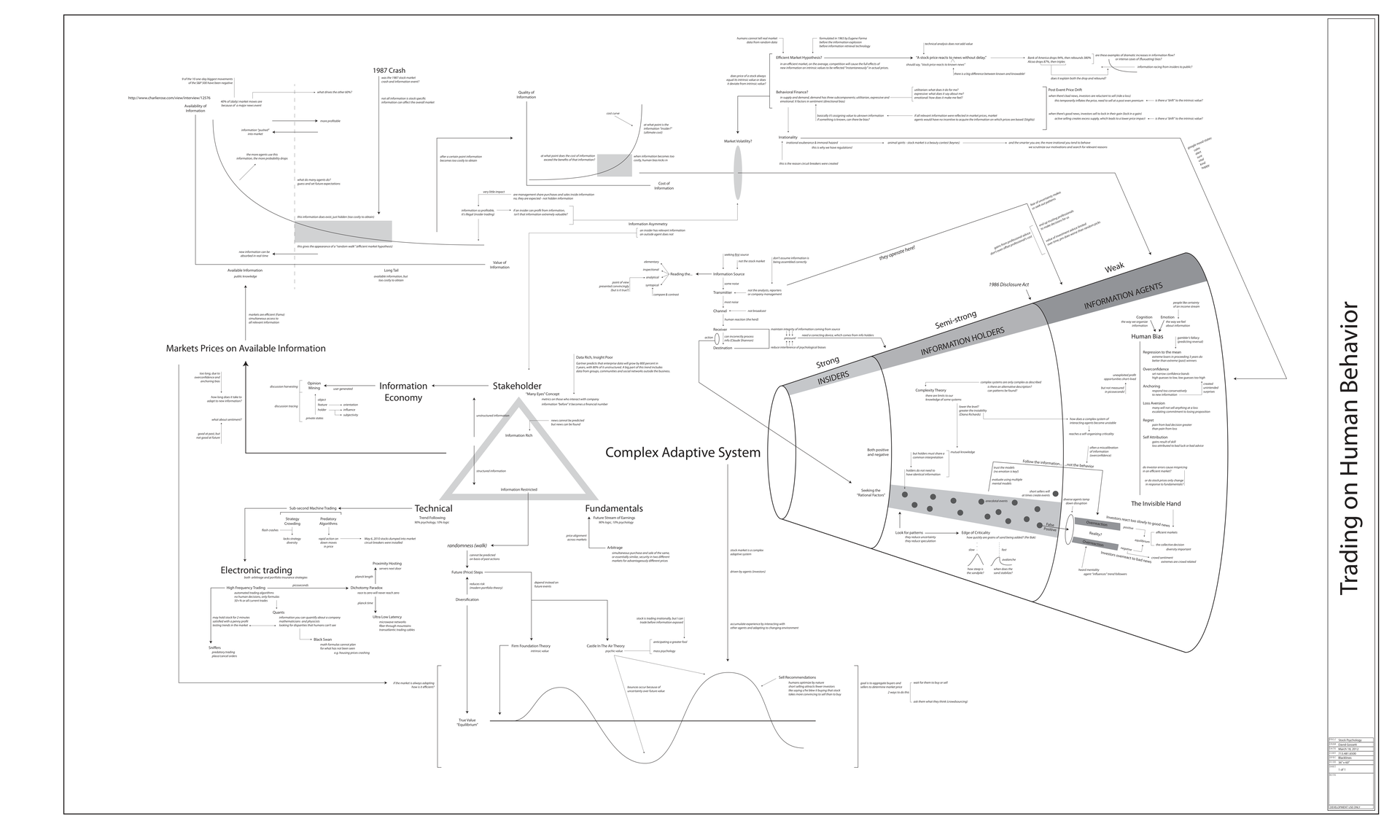

The Information Efficiency Spectrum:

This section examines how market prices process available information, tracing the flow from strong insiders to weak public agents. By analyzing information asymmetry, retrieval costs, and structural barriers, it highlights how unequal access drives volatility. Ultimately, the framework illustrates that markets struggle to maintain true equilibrium when critical data remains heavily concentrated, costly, or unevenly distributed.

|

Algorithmic Velocity and Systemic Risk:

Modern financial markets rely heavily on automated algorithmic execution, quantitative modeling, and predatory trading strategies. This digital paradigm prioritizes execution speed, creating a complex arena where microsecond advantages dictate overall profitability. However, these automated systems also introduce distinct systemic risks, including rapid flash crashes, machine feedback loops, and unexpected black swan events that challenge traditional economic models.

|

The Psychology of Market Adaptation:

This perspective frames financial systems as complex adaptive environments governed by human psychology and cognitive biases. Rational behavior is frequently disrupted by emotional responses like overconfidence, regret aversion, and herd mentality. These collective behavioral patterns prevent markets from acting as perfectly efficient processors, instead creating waves of overreaction, underreaction, and inevitable speculative bubbles driven by the crowd.

|