Engineering Off-Prime Credit:

The emergence of "off-prime" loan structures represents a critical shift in credit accessibility and financial engineering. By loosening traditional borrowing constraints, financial institutions enabled rapid market expansion but simultaneously introduced systemic fragility. This structural design prioritized short-term volume over long-term stability, establishing a highly volatile foundation for both individual consumers and the broader global financial marketplace.

|

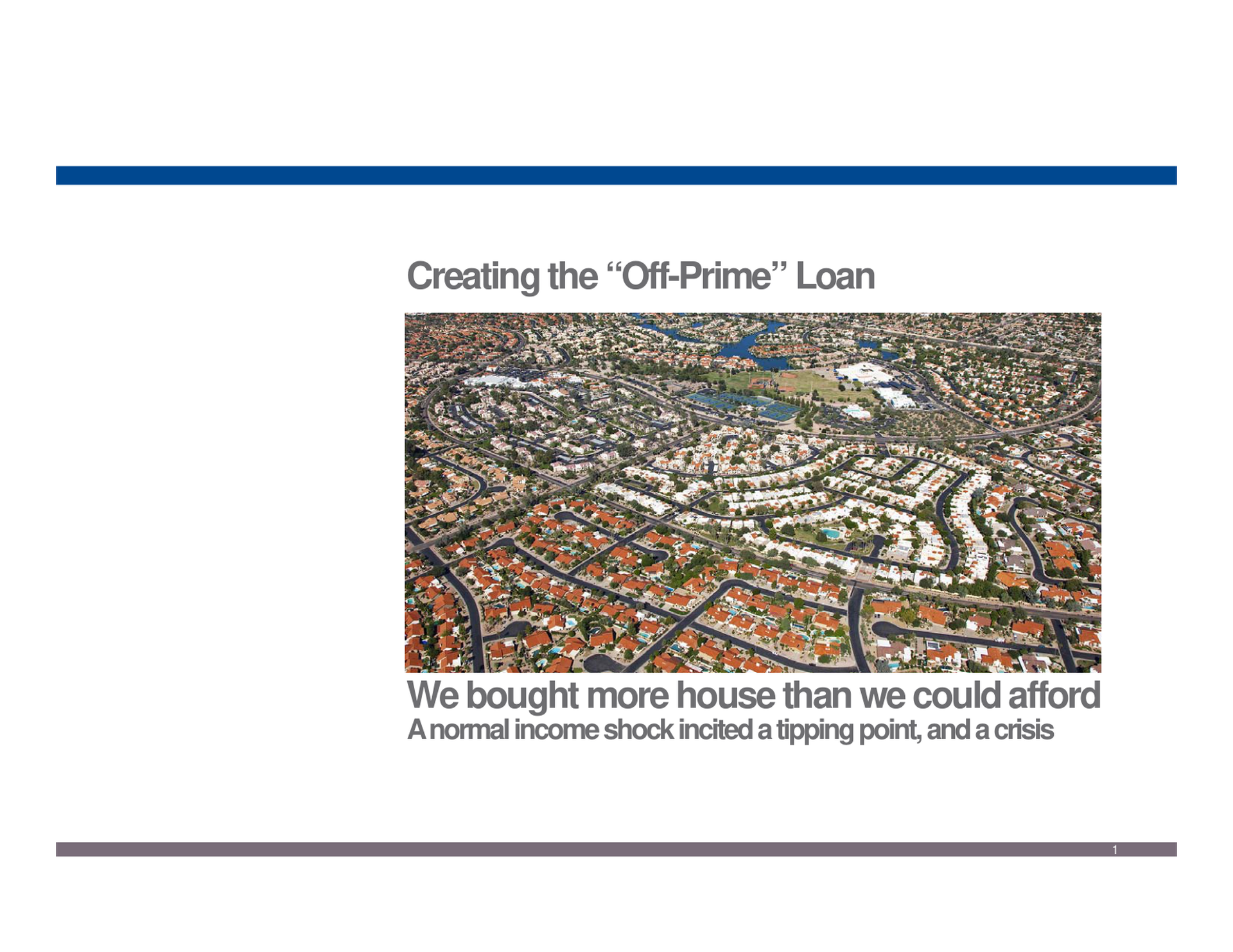

The Over-Leveraged Consumer:

Driven by low interest rates and optimistic market sentiments, consumers aggressively extended their purchasing power beyond sustainable levels. Buying more housing assets than household budgets could realistically support created a precarious economic reality. This widespread over-leveraging left suburban homeowners highly exposed, stripping away their financial safety nets and linking individual household decisions directly to macroscopic systemic vulnerabilities.

|

Catalysts of Systemic Collapse:

When household leverage is maximized, even minor or routine economic disruptions can trigger disproportionate damage. A standard income shock, normally manageable under balanced financial conditions, rapidly becomes a catastrophic tipping point in a highly leveraged environment. This initial disturbance quickly escalated into a widespread systemic crisis, demonstrating how interconnected localized debt vulnerabilities can destabilize the entire macroeconomic landscape.

|